California minimum auto insurance limits matter after every serious crash. Many drivers only think about insurance when they pay a bill. After an accident, those numbers can decide how much money is available for medical bills, lost wages, vehicle damage, and other losses.

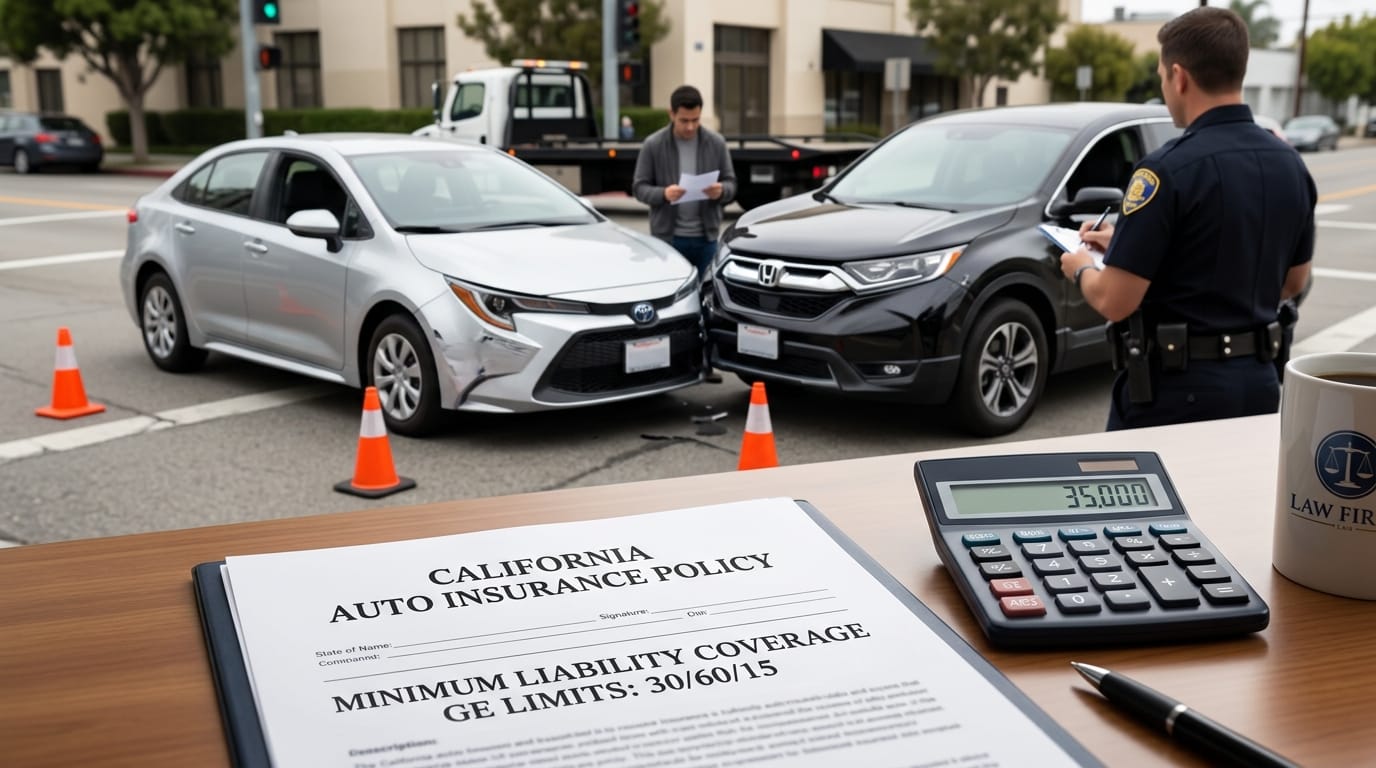

California’s current minimum liability limits are often called 30/60/15. That means $30,000 for injury or death to one person, $60,000 for injury or death to more than one person, and $15,000 for property damage. These limits apply to basic liability coverage for many California drivers.

The higher limits give accident victims more protection than the old limits. Still, they may not be enough after a major crash. One emergency room visit, ambulance ride, surgery, or hospital stay can use up coverage quickly. A crash involving several injured people can create even more pressure.

For injured victims, the key issue is simple. How much insurance is available, and what happens if the damages are higher than the policy limits? That question can shape the whole claim.

Why California Minimum Auto Insurance Limits Matter in 2026

California drivers must show financial responsibility. Most people do this through auto liability insurance. The California DMV lists the current minimum liability requirements as $30,000 for injury or death to one person, $60,000 for injury or death to more than one person, and $15,000 for property damage. Readers can review the official DMV page here: California DMV auto insurance requirements.

These limits matter because liability insurance pays other people when the insured driver causes a crash. It does not pay the at-fault driver for their own injuries. It protects injured victims up to the policy limit.

The California Department of Insurance also explains that standard auto policies now have higher minimum liability limits. That change improved basic protection. It did not make every crash fully covered. Readers can review the official insurance update here: California Department of Insurance auto insurance update.

A California minimum auto insurance limits case can become difficult when damages exceed coverage. That is common after serious crashes. The injured person may need to review every possible source of recovery.

What 30/60/15 actually means

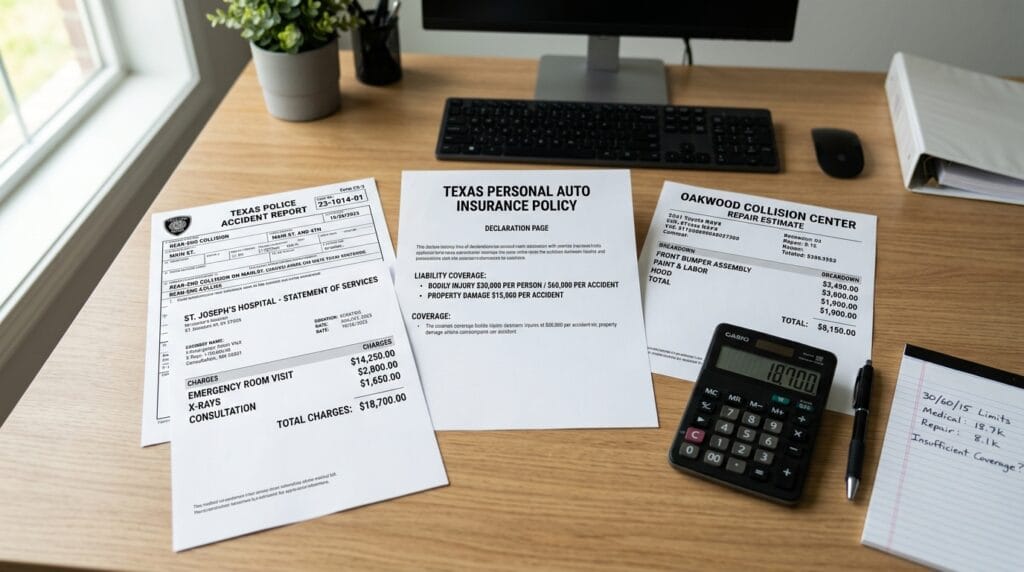

The first number is $30,000. That is the most the at-fault driver’s basic policy may pay for injury or death to one person. If one victim has $80,000 in medical bills, the minimum policy may not come close to covering the full loss.

The second number is $60,000. That is the total injury coverage for more than one injured person in the same crash. If three people get hurt, they may need to share that amount. This can create settlement disputes when several victims have strong claims.

The third number is $15,000. That applies to property damage. It may cover vehicle repairs, replacement value, or damage to other property. With today’s repair costs, even this amount can disappear fast.

Minimum coverage does not mean full compensation

Minimum coverage only creates a floor. It does not guarantee full payment. A victim may have damages far above the policy limit. That problem becomes worse when the injuries involve surgery, permanent pain, brain trauma, spinal injuries, fractures, or long recovery time.

Insurance companies may offer the policy limit and say that is all they can pay. Sometimes that is true for that policy. Other times, more coverage may exist. A victim should not assume the first policy found is the only available source.

Other possible sources may include the vehicle owner’s policy, employer coverage, commercial coverage, umbrella coverage, rideshare coverage, uninsured motorist coverage, or underinsured motorist coverage. The facts control the answer.

Several injured people may compete for the same limit

Multi-vehicle crashes can create serious insurance problems. If one at-fault driver carries minimum coverage and several people are hurt, the $60,000 per-accident limit may not cover everyone fairly.

For example, one crash may injure a driver, two passengers, and a pedestrian. Each person may have medical bills and pain. The insurance company may try to settle all claims within one limited pool of money.

Victims should avoid rushing into a low settlement. A fast offer may not reflect the full injury value. It may also fail to consider other policies. Once a release is signed, the claim usually ends against that party.

Underinsured motorist coverage can become important

Underinsured motorist coverage may help when the at-fault driver has insurance, but not enough. This coverage belongs to the injured person’s own policy. It can become important after a crash with a minimum-limit driver.

Many people do not know whether they have this coverage. Others have it but do not understand how it works. After a serious crash, victims should check their own auto policy. They should also review household policies when appropriate.

This issue often comes up when medical bills exceed the at-fault driver’s limits. It may also arise when the victim has lost wages, future care needs, or permanent injuries. Underinsured motorist coverage can help close the gap.

Do not assume the at-fault driver’s policy is the only source

The at-fault driver’s policy is only the starting point. More coverage may exist depending on who owned the vehicle, why the driver was on the road, and whether the crash involved work duties.

A delivery driver, company vehicle, rideshare trip, commercial vehicle, or borrowed car may create more insurance questions. Vehicle ownership can also matter. Sometimes the person driving is not the only person or business connected to the claim.

This is why early investigation matters. A victim should identify the driver, vehicle owner, employer, insurance carrier, and all possible coverage sources. Missing one policy can reduce recovery.

How Insurance Limits Affect Settlement Strategy

Policy limits can shape how a claim moves forward. If damages are clearly higher than available coverage, the injured person may need a policy-limit demand. That demand should include strong evidence of fault and damages.

A strong demand may include medical records, bills, wage loss proof, crash photos, police reports, witness statements, vehicle damage photos, and future treatment estimates. The goal is to show why the claim deserves payment up to the limit.

Insurance companies still review these claims carefully. They may dispute treatment, injury severity, lost wages, or fault. They may also argue comparative negligence. Your site already has a useful article on comparative negligence in car accident cases. That internal link fits well because fault percentages can reduce compensation.

Insurance communication also matters. Victims should be careful with adjusters. Your article on how attorneys handle insurance communication after accidents is a strong internal support link for this topic.

Evidence can increase pressure on the insurer

Evidence can make a policy-limit demand stronger. Clear liability helps. Severe injuries help. Consistent medical records help. Witnesses, videos, photos, and police reports can also increase pressure.

If the at-fault driver fled the scene, the claim may involve different insurance issues. Your site already has a guide on California hit-and-run accident claims. That article can help readers who need uninsured motorist guidance after a fleeing driver crash.

Speed evidence may also affect value. If the at-fault driver was speeding, the crash may have caused greater injuries. Your article on California speed safety camera accident claims can support readers who need more evidence-based information.

Do not settle before the full damage picture is clear

A quick settlement can create a serious problem. Early offers may arrive before the victim understands the full injury. Pain may worsen. Doctors may order imaging. Surgery may become necessary. Work restrictions may last longer than expected.

Before settling, victims should review medical bills, future care, lost wages, pain and suffering, vehicle damage, and long-term limits. They should also confirm all insurance sources. A minimum policy limit does not always mean the investigation should stop.

Victims should avoid giving broad recorded statements without preparation. Adjusters may ask questions that reduce value. They may ask the victim to guess about speed, distance, prior pain, or fault. Guessing can hurt the claim.

California minimum auto insurance limits provide important protection, but they do not guarantee full recovery after a serious crash. The 30/60/15 limits can help more than the old limits, yet major injuries can still exceed basic coverage fast.

If you were injured in a California car crash, review every coverage source before signing anything. Get medical care, document your injuries, preserve evidence, avoid rushed statements, and make sure the claim accounts for future damages. For more legal guidance, visit the Auto Accident Lawyer services page or explore the auto accident blog.